Retirement as Americans know it is retiring. With workers transitioning from a system of defined benefits, i.e. pensions, to one of defined contributions like 401(k)s and IRAs, the burden of retirement planning is shifting more and more heavily to the individual—but has this demand for personal responsibility translated to meaningful action?

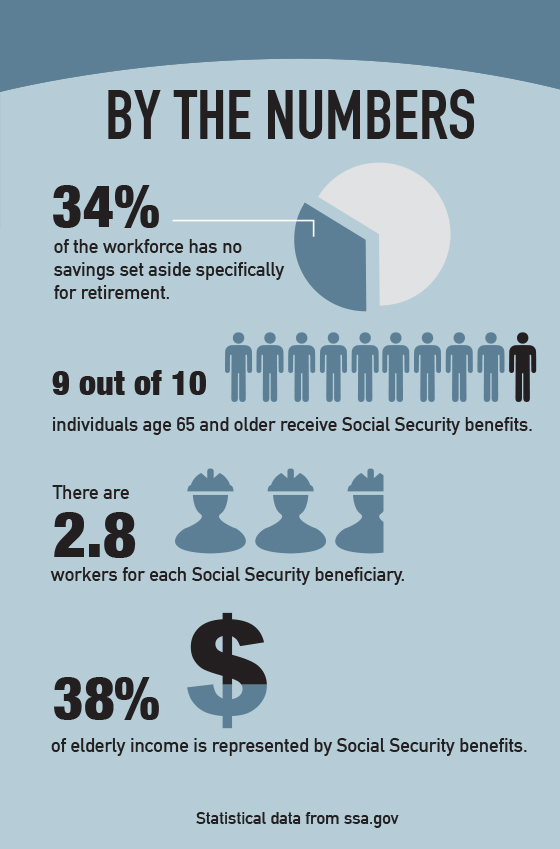

Social Security benefits constituted the only retirement savings for nearly a third of non-retirees who responded to a survey conducted for the Report on the Economic Well-Being of U.S. Households in 2014, including 25 percent of respondents age 60 and older who reported no retirement savings outside of Social Security benefits. While about 65 percent of respondents said they expected Social Security as a source of retirement income, 39 percent of non-retirees reported giving little or no thought to financial planning for retirement.

Although intentionally simple, however, Social Security poses unique questions worthy of thoughtful consideration.

Common Questions

“When to start taking Social Security is a big question and varies with each individual and their situation,” says Dick Besnier, investment advisor representative and president of Besnier Financial Group, Inc. in Williamsburg, Virginia. “I try and get people to delay taking Social Security unless they have no other source and need the income.”

Jayne Di Vincenzo, president of Lions Bridge Financial Advisors in Newport News, Virginia, agrees with delaying as long as possible. “The break-even point is living to 80 for most beneficiaries,” she says. “If you have longevity in your family, are in good health and have other sources of income to meet your needs, delay taking benefits if you can wait.”

Spousal benefits are another concern and tie into deciding when to collect, says Besnier. The main reason he encourages delaying collecting as long as possible, he says, is to maximize the benefit of the surviving spouse. One strategy, which Besnier cautions is not appropriate for everyone, is filing and suspending when both spouses reach their respective full retirement age, which varies based on year born. This enables the couple to receive half of their larger benefit while accumulating delayed retirement credits until age 70.

Collecting Early

Collecting benefits early may be appropriate in some cases, according to John Pawlowski, president of Norseman Advisory Group Inc. in Newport News, Virginia. “If you need it to retire, your health isn’t great, you hate your boss or your job, or any other reason you feel is important, you paid into it and you earned the benefit,” he says. “Take it when you need to.”

However, Pawlowski warns that you should be aware of benefits you may sacrifice when collecting early, especially if married. “If you are the higher wage earner, and you are married, remember you are making a decision for both you and your spouse with regard to survivor benefits,” he says, explaining that the surviving spouse receives the higher of the couple’s benefits.

Age-based Expectations

Survey findings from the Report on the Economic Well-Being of U.S. Households in 2014 may indicate concern over the long-term efficacy of the Social Security program among younger Americans; 92 percent of respondents age 60 and older anticipated Social Security benefits as retirement income compared to 44 percent of respondents age 30 and younger.

Whether this indicates younger non-retirees think less actively about Social Security than their older cohorts or represents concern over the program’s future solvency is unclear, the report noted, though Besnier said he believes younger workers are troubled.

“Unfortunately, the people in that age group don’t feel confident that [Social Security] will be around,” says Besnier. “I do recognize there are concerns, but I truly believe adjustments will be made to make sure the program continues.” Pawlowski shares Besnier’s optimism, saying he believes Social Security benefits will be “an integral part of our American retirement culture well into the future.”